Cheapest Car Brands To Insure: A Comprehensive Guide to Saving on Your Premiums

Cheapest Car Brands To Insure: A Comprehensive Guide to Saving on Your Premiums cars.truckstrend.com

Owning a car involves more than just the initial purchase price; it encompasses fuel, maintenance, and, crucially, insurance. Car insurance is a mandatory expense for most drivers, and its premiums can significantly impact your overall cost of vehicle ownership. While many factors influence your insurance rates, one of the most substantial yet often overlooked is the specific car brand and model you choose. Understanding which car brands are generally cheaper to insure can lead to substantial savings over the lifetime of your vehicle.

This comprehensive guide delves into the world of affordable car insurance, exploring the factors that drive premiums and highlighting the car brands and models that consistently offer lower rates. By making an informed decision before you buy, you can put yourself in the driver’s seat of long-term savings.

Cheapest Car Brands To Insure: A Comprehensive Guide to Saving on Your Premiums

Understanding What Drives Insurance Premiums

Before we dive into specific brands, it’s essential to grasp the underlying factors that insurance companies consider when calculating your premium. These factors primarily revolve around risk assessment – how likely is your vehicle to be involved in an accident, stolen, or cost a lot to repair?

Vehicle-Specific Factors:

- Safety Ratings: Cars with excellent crash test ratings (e.g., from IIHS Top Safety Pick or NHTSA 5-star ratings) and advanced safety features (like automatic emergency braking, lane-keeping assist) are often cheaper to insure. They reduce the risk of severe injuries in a collision, lowering potential payout for medical claims and often preventing accidents altogether.

- Repair Costs & Parts Availability: Vehicles that are expensive to repair, require specialized tools, or have costly, hard-to-find parts (especially imported components) will typically have higher insurance premiums. Cars with widely available, affordable parts and straightforward repair processes are more economical for insurers.

- Theft Rates: Models that are frequently stolen are deemed higher risk, leading to higher comprehensive coverage premiums. Insurers track theft data closely.

- Engine Size & Horsepower: More powerful, high-performance vehicles are often associated with higher speeds and more aggressive driving, increasing the likelihood and severity of accidents. Economy cars with smaller engines usually incur lower premiums.

- Vehicle Value: The higher the market value of your car, the more it will cost to replace if it’s totaled or stolen, and the more expensive its repairs will be. Therefore, less expensive cars typically have lower comprehensive and collision premiums.

- Likelihood of Damage: Certain vehicle designs (e.g., low-slung sports cars) might be more prone to damage in minor incidents like hitting a curb.

Driver-Specific Factors (Briefly for Context):

While our focus is on car brands, remember that your personal profile also plays a huge role:

- Driving Record: Accidents and traffic violations significantly increase rates.

- Age and Experience: Young, inexperienced drivers typically pay more.

- Location: Urban areas with high traffic density and theft rates often have higher premiums.

- Credit Score: In many states, a good credit score can lead to lower rates.

- Deductible & Coverage Limits: Higher deductibles mean lower premiums, and more comprehensive coverage costs more.

Top Contenders: Car Brands Generally Cheaper to Insure

Based on the factors above, certain car brands consistently emerge as more affordable to insure. These are typically brands known for reliability, safety, widespread parts availability, and a demographic of drivers who tend to be more cautious.

- Toyota: Often hailed as the king of reliability, Toyota vehicles like the Corolla, Camry, and RAV4 are perennial favorites for low insurance costs. Their excellent safety ratings, low theft rates, widespread parts availability, and reputation for durability contribute to lower premiums. They are often driven by a wide demographic, including many conservative drivers.

- Honda: Similar to Toyota, Honda models such as the Civic (non-performance trims), CR-V, and Accord are excellent choices. They boast strong safety features, high reliability, and a vast network for parts and service, making them inexpensive for insurers to cover.

- Subaru: While all-wheel drive (AWD) might suggest higher costs, Subaru’s exceptional safety ratings (often a Top Safety Pick+ from IIHS), robust construction, and lower theft rates for models like the Impreza, Forester, and Crosstrek often translate to surprisingly affordable insurance. Their AWD system is also perceived to reduce accident risk in adverse conditions.

- Hyundai & Kia: In recent years, Hyundai and Kia have made significant strides in safety, reliability, and technology. Models like the Hyundai Elantra, Kona, Kia Forte, and Soul offer good value, come with strong warranties, and benefit from increasingly accessible parts and repair networks, leading to competitive insurance rates.

- Nissan: Nissan’s more economical models, such as the Sentra and Rogue, tend to be cheaper to insure. They offer affordability, widely available parts, and decent safety features, appealing to budget-conscious drivers.

- Chevrolet & Ford (Select Models): While American muscle cars or large trucks from these brands can be expensive to insure, their more common, mass-market sedans and compact SUVs often offer competitive rates. Models like the Chevrolet Malibu or Ford Escape benefit from widespread parts availability and a large service network, keeping repair costs down for insurers.

Why These Brands (and Specific Models) Stand Out

The common thread among these brands and their cheapest-to-insure models is a combination of the following:

- High Safety Scores: They consistently perform well in crash tests, leading to fewer severe injuries and lower medical payouts.

- Low Theft Rates: They are less frequently targeted by thieves compared to luxury or high-performance vehicles.

- Affordable and Available Parts: Their parts are widely manufactured and easily accessible, reducing repair costs and time.

- Reliability and Durability: Less frequent breakdowns or mechanical issues mean fewer claims related to comprehensive coverage or towing.

- Driver Demographics: These cars are often purchased by a broad range of drivers, including many who prioritize safety and practicality over speed, and tend to have cleaner driving records.

- Lower Performance Profiles: Most models within these brands (especially the base trims) are not designed for high speed or aggressive driving, reducing the perceived risk of high-speed collisions.

It’s crucial to remember that even within these "cheap to insure" brands, specific models and trims can vary significantly. A Honda Civic Type R, for instance, will be far more expensive to insure than a base Honda Civic LX. The key is often to stick to economy, compact, or mid-size sedans and small to mid-size SUVs.

Practical Advice and Actionable Insights

Choosing a car that’s cheap to insure is a smart financial move. Here’s how to apply this knowledge:

- Get Quotes Before You Buy: This is the golden rule. Before finalizing a car purchase, get insurance quotes for the exact make, model, and trim level you are considering from multiple insurance providers. A seemingly great deal on a car can quickly be negated by sky-high insurance premiums.

- Consider the Total Cost of Ownership: Don’t just look at the sticker price. Factor in insurance, fuel efficiency, maintenance, and potential resale value when evaluating a vehicle.

- Prioritize Safety Features: When comparing models, opt for vehicles with advanced driver-assistance systems (ADAS) like automatic emergency braking, lane departure warning, and adaptive cruise control. Many insurers offer discounts for these features.

- New vs. Used: While newer cars might have higher replacement costs, they often come with advanced safety features that can offset some of the cost. Older cars (without significant safety tech) might have cheaper comprehensive/collision coverage if their value is low, but liability remains.

- Avoid Performance Trims: If you’re aiming for low insurance, steer clear of "sport," "turbo," or "performance" variants of otherwise affordable models.

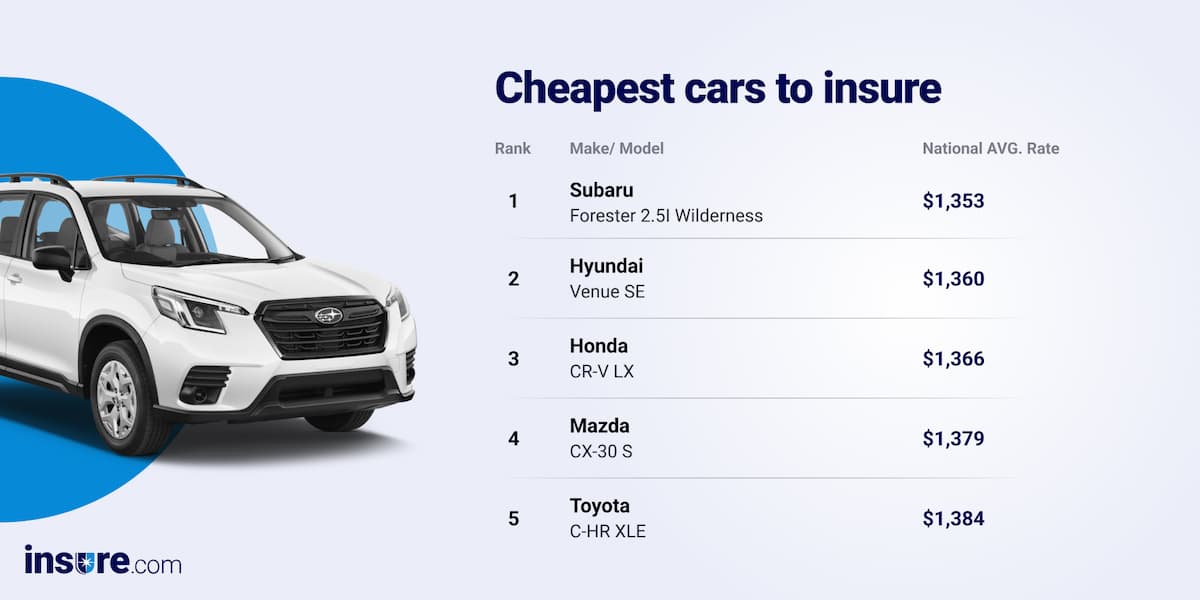

Table: Estimated Annual Insurance Costs for Cheapest Car Brands & Models

The following table provides estimated average annual insurance costs for some of the consistently cheapest car brands and models to insure. Please note that these figures are estimates based on a hypothetical average driver profile (30-45 years old, clean record, good credit, full coverage, suburban location) and are subject to significant variation based on individual circumstances, location, specific policy details, and current market conditions.

| Car Brand & Model | Typical Body Style | Key Factors for Lower Insurance | Estimated Average Annual Insurance Cost (USD) | Notes |

|---|---|---|---|---|

| Toyota Corolla (LE/SE) | Compact Sedan | Legendary Reliability, Low Repair Costs, High Safety, Low Theft | $1,400 – $1,700 | A benchmark for low insurance costs due to its all-around low risk profile. |

| Honda Civic (LX/EX) | Compact Sedan/Hatch | High Safety, Reliability, Low Theft, Affordable Parts | $1,500 – $1,800 | Very popular, widely available parts, excellent safety ratings. |

| Hyundai Elantra (SE/SEL) | Compact Sedan | Good Safety Ratings, Affordable Parts, Value, Improved Reliability | $1,450 – $1,750 | Significant improvements in recent years make it a strong contender for affordability. |

| Kia Forte (LX/GT-Line) | Compact Sedan | Value, Strong Warranty, Improving Safety Features | $1,450 – $1,750 | Shares many characteristics with the Elantra, offering great value for money. |

| Nissan Sentra | Compact Sedan | Affordability, Common Parts, Reliability, Low Performance | $1,450 – $1,750 | A no-frills choice often with lower premiums due to its practical nature. |

| Subaru Impreza (Base/Premium) | Compact Sedan/Hatch | AWD Safety, Good Reliability, High Safety Ratings | $1,500 – $1,800 | AWD system contributes to perceived safety, consistently high safety ratings. |

| Toyota Camry (LE/SE) | Mid-size Sedan | Reliability, Safety, Common Parts, Lower Theft | $1,550 – $1,850 | Similar benefits to Corolla, but slightly higher due to vehicle value and size. |

| Honda CR-V | Compact SUV | High Safety, Reliability, Family-Oriented, Popularity | $1,600 – $1,900 | One of the best-selling SUVs, known for its safety and practicality. |

| Subaru Forester | Compact SUV | AWD Safety, Reliability, Family Focus, High Safety Ratings | $1,600 – $1,900 | A solid choice for families, strong in safety and versatility. |

| Toyota RAV4 | Compact SUV | High Safety, Reliability, Popularity, Parts Availability | $1,650 – $1,950 | Another top-selling SUV, benefits from Toyota’s reputation for reliability and safety. |

| Chevrolet Malibu (LS/LT) | Mid-size Sedan | Common Parts, Domestic Production, Value, Widespread Service | $1,500 – $1,800 | A practical domestic sedan, widely available parts keep repair costs down. |

| Ford Escape | Compact SUV | Popularity, Parts Availability, Good Safety Ratings | $1,600 – $1,900 | A common sight on roads, benefiting from a large parts and service network. |

Frequently Asked Questions (FAQ)

Q1: Are luxury cars always more expensive to insure?

A1: Generally, yes. Luxury cars typically have higher purchase prices, more expensive and specialized parts, advanced technology that costs more to repair, and are often targets for theft. All these factors contribute to higher insurance premiums.

Q2: Does the color of my car affect insurance?

A2: No, the color of your car does not directly affect your insurance rates. This is a common myth. Insurers care about the make, model, year, safety features, engine size, and theft rates, not the paint color.

Q3: Does a car’s age affect insurance costs?

A3: Yes, a car’s age can affect insurance costs. Newer cars generally cost more to insure for comprehensive and collision coverage due to their higher replacement value. However, older cars might lack modern safety features, which could lead to higher liability or medical payments coverage if they’re deemed riskier in an accident. Also, very old cars might have higher repair costs if parts are scarce.

Q4: Why do some identical models have different insurance costs for different people?

A4: Insurance costs are highly individualized. Factors like your driving record, age, gender, location, credit score, marital status, chosen deductible, coverage limits, and even whether you bundle policies (home and auto) all significantly impact your premium.

Q5: Can I get cheaper insurance if my car has advanced safety features?

A5: Absolutely! Many insurance companies offer discounts for vehicles equipped with advanced driver-assistance systems (ADAS) like automatic emergency braking, lane-keeping assist, adaptive cruise control, blind-spot monitoring, and anti-theft devices. These features can reduce the likelihood of accidents or theft, benefiting both you and the insurer.

Q6: Is it true that red cars cost more to insure?

A6: No, this is a pervasive myth. Car color has no bearing on insurance rates. Insurers are interested in the vehicle’s risk profile, not its aesthetic.

Conclusion

Choosing a car that is inexpensive to insure is a smart financial strategy that can yield significant savings over time. By understanding the factors that influence insurance premiums – primarily safety, reliability, repair costs, and theft rates – you can make an informed decision. Brands like Toyota, Honda, Subaru, Hyundai, Kia, Nissan, and select models from Chevrolet and Ford consistently offer lower insurance rates due to their strong safety records, widespread parts availability, and practical design.

Remember, the true cost of car ownership extends far beyond the showroom floor. By taking a holistic approach and considering insurance premiums as a vital component of your budget, you can ensure your dream car doesn’t turn into a financial burden. Always get multiple insurance quotes before making a purchase, and drive safely to keep those premiums low.