Cheapest Car Brands To Insure: A Comprehensive Guide to Affordable Auto Insurance

Cheapest Car Brands To Insure: A Comprehensive Guide to Affordable Auto Insurance cars.truckstrend.com

Owning a car is a necessity for many, but the cost doesn’t end with the purchase price. Auto insurance is a significant ongoing expense that can vary wildly depending on numerous factors, chief among them being the specific make and model of your vehicle. For budget-conscious consumers, understanding which car brands generally offer the cheapest insurance rates can translate into substantial savings over the lifetime of their vehicle.

This comprehensive guide will delve into the world of affordable auto insurance, exploring the factors that influence premiums and highlighting the car brands and models that consistently rank as the cheapest to insure. By arming yourself with this knowledge, you can make an informed decision that saves you money long before you even hit the road.

Cheapest Car Brands To Insure: A Comprehensive Guide to Affordable Auto Insurance

Understanding Car Insurance Premiums: The Key Factors Beyond Your Driving Record

Before we pinpoint specific brands, it’s crucial to grasp what influences your car insurance premiums. Insurers calculate risk, and that risk assessment is based on a complex algorithm of variables. While your personal driving record, age, location, and credit score play a significant role, the car itself is a major determinant. Here are the primary vehicle-related factors:

- Vehicle Make, Model, and Year: Different cars have different risk profiles. A high-performance sports car will almost always cost more to insure than a modest family sedan. Newer cars often cost more to insure than older ones due to higher replacement values and more expensive repair technologies.

- Safety Features and Ratings: Cars with excellent safety ratings (e.g., from the IIHS and NHTSA) and advanced safety features (like automatic emergency braking, lane-keeping assist, and multiple airbags) are less likely to result in serious injuries or fatalities in an accident. This reduces the insurer’s potential payout for medical claims, often leading to lower premiums.

- Repair Costs and Parts Availability: Vehicles that are expensive to repair or require specialized, hard-to-find parts will typically have higher insurance costs. This is especially true for luxury or imported vehicles. Cars with common, readily available, and affordable parts are cheaper to fix after an accident, translating to lower comprehensive and collision premiums.

- Theft Rates: If a particular car model is frequently stolen, insurers will charge more for comprehensive coverage (which covers theft). Cars with effective anti-theft devices or those less desirable to thieves will typically see lower premiums.

- Engine Size and Performance: Vehicles with powerful engines and high horsepower are statistically more likely to be involved in accidents due to their potential for higher speeds and more aggressive driving. Insurers view these as higher-risk vehicles.

- Likelihood of Accidents: Some vehicles, regardless of their safety features, might be statistically more prone to being involved in accidents. This could be due to their typical driver demographic or design.

Top Contenders: Car Brands Generally Cheaper to Insure

While "cheapest" is always relative to individual circumstances, certain car brands and their popular models consistently appear on lists of vehicles with lower average insurance premiums. These brands tend to share common characteristics: reliability, excellent safety ratings, lower repair costs, and a generally less "sporty" or "high-performance" image.

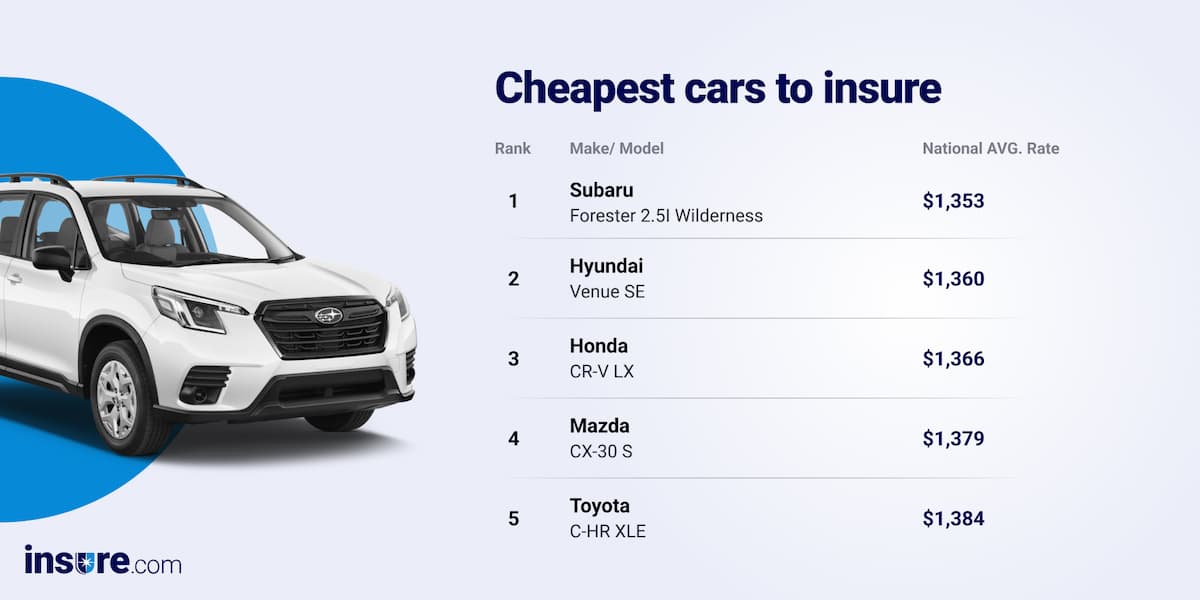

- Subaru: Known for their standard all-wheel drive and strong safety ratings, models like the Forester, Outback, and Crosstrek are often among the cheapest to insure. Their reputation for reliability and driver loyalty also plays a role.

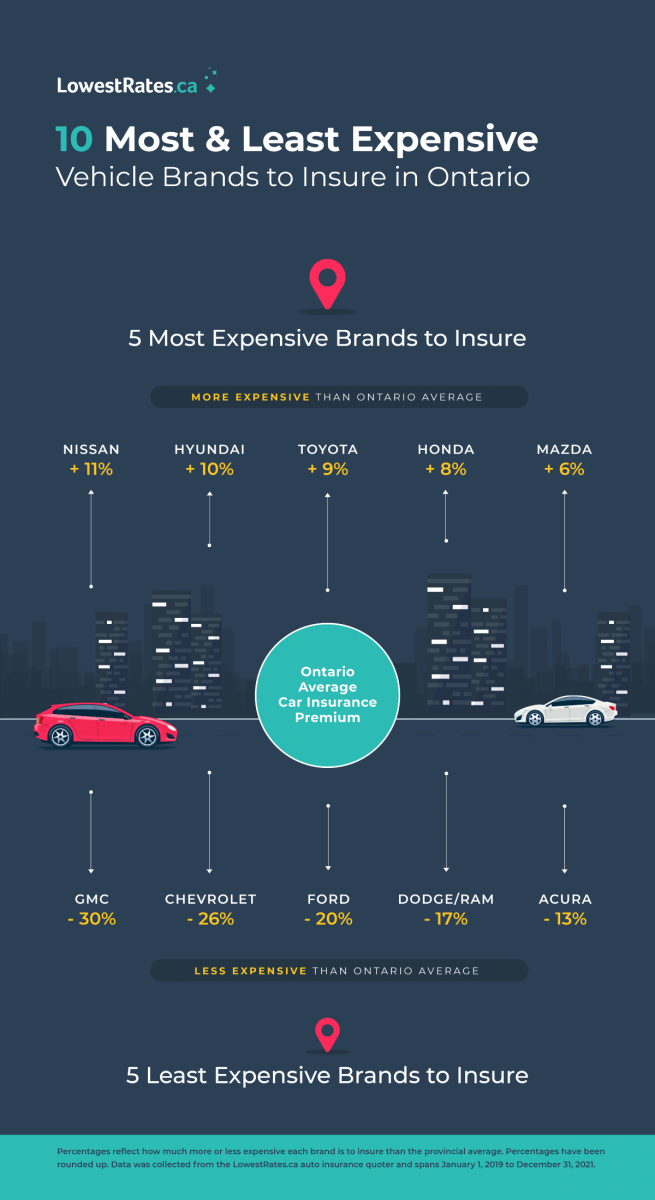

- Honda: A perennial favorite for affordability and reliability. The Honda Civic and CR-V are consistently lauded for their low insurance costs. They are safe, popular, and parts are widely available.

- Toyota: Similar to Honda, Toyota’s reputation for bulletproof reliability, excellent safety features, and widespread availability of parts makes models like the Corolla, Camry, and RAV4 highly insurable at reasonable rates.

- Mazda: While sometimes overlooked, Mazda has made significant strides in safety and reliability. Models like the Mazda3 and CX-5 often offer competitive insurance rates, especially given their engaging driving dynamics.

- Kia: Having shed its "cheap car" image for one of quality and value, Kia models like the Forte, Soul, and Sportage often boast good safety ratings and reasonable repair costs, contributing to lower insurance premiums.

- Hyundai: Hyundai, Kia’s sister brand, also offers competitive insurance rates on models like the Elantra, Sonata, and Tucson. Their strong warranty, improving safety features, and affordability make them attractive.

- Volkswagen: For those seeking a European feel without the premium insurance costs, Volkswagen models like the Jetta and Tiguan can be surprisingly affordable to insure due to their solid safety scores and moderate performance.

- Ford: While Ford offers a wide range of vehicles, popular models like the Focus (when available new), Escape, and Fusion often have reasonable insurance costs due to their widespread availability, parts commonality, and generally good safety.

- Chevrolet: Similar to Ford, Chevrolet’s mainstream sedans and SUVs, such as the Malibu and Equinox, tend to be more affordable to insure than their performance-oriented counterparts.

Why These Brands (and Models) Are More Affordable to Insure

The common threads running through the brands listed above provide a clear picture of what insurers look for:

- Exceptional Safety Ratings: Cars from these brands frequently earn "Top Safety Pick" awards from the IIHS and 5-star ratings from the NHTSA. Fewer serious injuries mean lower medical payouts for insurers.

- High Reliability and Lower Repair Costs: These vehicles are known for their dependability, meaning fewer breakdowns and less frequent repairs. When repairs are needed, parts are often common, making them cheaper and quicker to source.

- Lower Theft Rates: While no car is immune to theft, mainstream sedans and SUVs from these brands are generally less targeted by professional car thieves than luxury cars or high-performance vehicles, which translates to lower comprehensive coverage costs.

- Moderate Performance: Most models from these brands are not designed for extreme speed or performance. Their more practical nature means they are statistically less likely to be involved in high-speed, high-impact accidents.

- Market Saturation and Parts Availability: Due to their popularity, parts for these vehicles are widely manufactured and easily accessible, reducing the cost of repairs after an accident.

Practical Tips for Finding the Cheapest Insurance

Even if you choose a car from one of the "cheapest to insure" brands, your individual efforts can further reduce your premiums.

- Shop Around Extensively: Never settle for the first quote. Get quotes from at least 3-5 different insurance providers (e.g., State Farm, GEICO, Progressive, Allstate, local independent agents). Prices can vary by hundreds of dollars for the exact same coverage.

- Bundle Policies: If you have homeowner’s or renter’s insurance, bundle it with your auto policy from the same provider for a multi-policy discount.

- Increase Your Deductible: Opting for a higher deductible (e.g., $1,000 instead of $500) will lower your premium, but ensure you can afford to pay that amount out-of-pocket if you need to file a claim.

- Maintain a Clean Driving Record: Avoid accidents and traffic violations. A spotless record is the single best way to keep your premiums low.

- Ask About Discounts: Many insurers offer a plethora of discounts: good student, low mileage, anti-theft devices, multi-car, safe driver programs (telematics), military, professional affiliations, and more. Always ask what you qualify for.

- Improve Your Credit Score: In most states, your credit-based insurance score significantly impacts your premium. A higher score generally leads to lower rates.

- Consider Telematics Programs: Many insurers offer programs that track your driving habits (speed, braking, mileage). Safe drivers can earn significant discounts.

- Review Coverage Levels Annually: As your car ages, you might consider dropping comprehensive and collision coverage if its market value no longer justifies the cost of the premium.

Challenges and Considerations

While aiming for the cheapest car to insure is a smart financial move, remember these points:

- "Cheapest" is Individual: The absolute cheapest car for one person might not be for another, due to personal factors like age, driving history, and location.

- Trim Levels and Options Matter: A base model of a car will almost always be cheaper to insure than its higher-trim, more powerful, or feature-laden counterpart.

- New vs. Used: Older vehicles generally cost less to insure because their replacement value is lower. However, older cars might lack modern safety features, which could slightly offset some savings.

- Beyond Insurance Costs: Don’t let insurance be the only factor. Consider the car’s reliability, fuel efficiency, maintenance costs, and how well it meets your needs and lifestyle. A car that’s cheap to insure but constantly breaks down isn’t a good deal.

Estimated Average Annual Insurance Premiums for Common "Cheapest" Models

Please note: These figures are illustrative estimates and vary significantly based on individual driver profiles (age, location, driving record, credit score), specific vehicle trim levels, chosen coverage amounts, and the insurance provider. They are intended to show relative affordability.

| Car Brand | Model (Common Trim) | Estimated Annual Premium Range | Key Reason for Lower Premium |

|---|---|---|---|

| Subaru | Forester | $1,300 – $1,700 | High Safety Ratings, Reliability |

| Subaru | Crosstrek | $1,250 – $1,650 | High Safety Ratings, Reliability |

| Honda | Civic | $1,350 – $1,800 | Reliability, Low Theft, Parts Availability |

| Honda | CR-V | $1,300 – $1,750 | Reliability, Safety, Popularity |

| Toyota | Corolla | $1,300 – $1,750 | Reliability, Safety, Low Theft |

| Toyota | RAV4 | $1,350 – $1,800 | Reliability, Safety, Popularity |

| Mazda | Mazda3 | $1,300 – $1,700 | Good Safety, Reliability |

| Mazda | CX-5 | $1,350 – $1,750 | Good Safety, Reliability |

| Kia | Forte | $1,300 – $1,700 | Good Safety, Value, Parts Availability |

| Kia | Sportage | $1,350 – $1,750 | Good Safety, Value |

| Hyundai | Elantra | $1,300 – $1,700 | Good Safety, Value, Parts Availability |

| Hyundai | Tucson | $1,350 – $1,750 | Good Safety, Value |

| Volkswagen | Jetta | $1,350 – $1,750 | Good Safety, Moderate Performance |

| Ford | Escape | $1,400 – $1,800 | Popularity, Parts Availability |

| Chevrolet | Malibu | $1,400 – $1,800 | Popularity, Parts Availability |

Conclusion

Choosing a car brand that is generally cheaper to insure can be one of the smartest financial decisions you make when purchasing a vehicle. Brands like Honda, Toyota, Subaru, and Mazda consistently offer lower premiums due to their strong safety records, reliability, and affordable repair costs. However, remember that your personal profile significantly impacts your final premium.

By combining the selection of a "low-insurance" vehicle with smart shopping practices – comparing quotes, leveraging discounts, and maintaining a clean driving record – you can significantly reduce your annual auto insurance expenses. Do your homework, ask the right questions, and drive away with savings that last for years to come.

Frequently Asked Questions (FAQ)

Q1: What is the single cheapest car to insure in the U.S.?

A1: There isn’t one single answer, as "cheapest" depends heavily on your individual profile (age, location, driving history, credit score). However, models like the Subaru Forester, Honda CR-V, Toyota RAV4, and their sedan counterparts (Civic, Corolla) consistently rank among the lowest average insurance costs due to their safety, reliability, and low theft rates.

Q2: Do electric cars cost more or less to insure?

A2: Generally, electric cars (EVs) tend to cost more to insure than comparable gasoline-powered vehicles. This is primarily due to higher repair costs for specialized components like batteries and electric motors, and sometimes a higher purchase price. However, as EV technology becomes more mainstream and repair infrastructure improves, these costs may decrease.

Q3: Does the color of my car affect my insurance rates?

A3: No, the color of your car has absolutely no bearing on your insurance rates. This is a common myth. Insurers are concerned with factors like the car’s make, model, year, safety features, repair costs, and theft rates, not its paint job.

Q4: How often should I compare car insurance quotes?

A4: It’s advisable to compare quotes at least once a year, or whenever a significant life event occurs (e.g., getting married, moving, buying a new car, improving your credit score, or having a child turn driving age). Insurers frequently update their algorithms and offer new discounts, so shopping around can always uncover savings.

Q5: Does my credit score affect my car insurance rates?

A5: Yes, in most states, your credit-based insurance score is a significant factor in determining your premium. Insurers use these scores as a predictor of how likely you are to file a claim. A higher credit score generally leads to lower insurance rates.

Q6: Is it always cheaper to insure an older car?

A6: Generally, yes. Older cars have a lower market value, which means the cost to repair or replace them after an accident is less for the insurer. However, an extremely old or rare classic car might be an exception, as specialized parts and maintenance can make them expensive to insure. Also, older cars may lack modern safety features, which could slightly offset some savings.