How To Buy A Brand New Car With Bad Credit

How To Buy A Brand New Car With Bad Credit cars.truckstrend.com

The dream of driving a brand new car, with that intoxicating "new car smell" and the latest technology, often feels out of reach when your credit score is less than stellar. Many believe that bad credit automatically disqualifies them from purchasing a new vehicle, relegating them to the used car market or no car at all. However, this isn’t necessarily true. While it presents unique challenges, buying a brand new car with bad credit is entirely possible with the right approach, diligent preparation, and a clear understanding of the financial landscape.

This comprehensive guide will walk you through the process, offering practical advice and actionable insights to help you navigate the complexities of securing a new car loan despite a less-than-perfect credit history. It’s about empowering you with the knowledge to make informed decisions and transform what seems like an impossible feat into a tangible reality.

How To Buy A Brand New Car With Bad Credit

Understanding Bad Credit and Its Impact on Car Loans

Before diving into the "how-to," it’s crucial to understand what "bad credit" means in the context of car loans and why it affects lenders’ decisions.

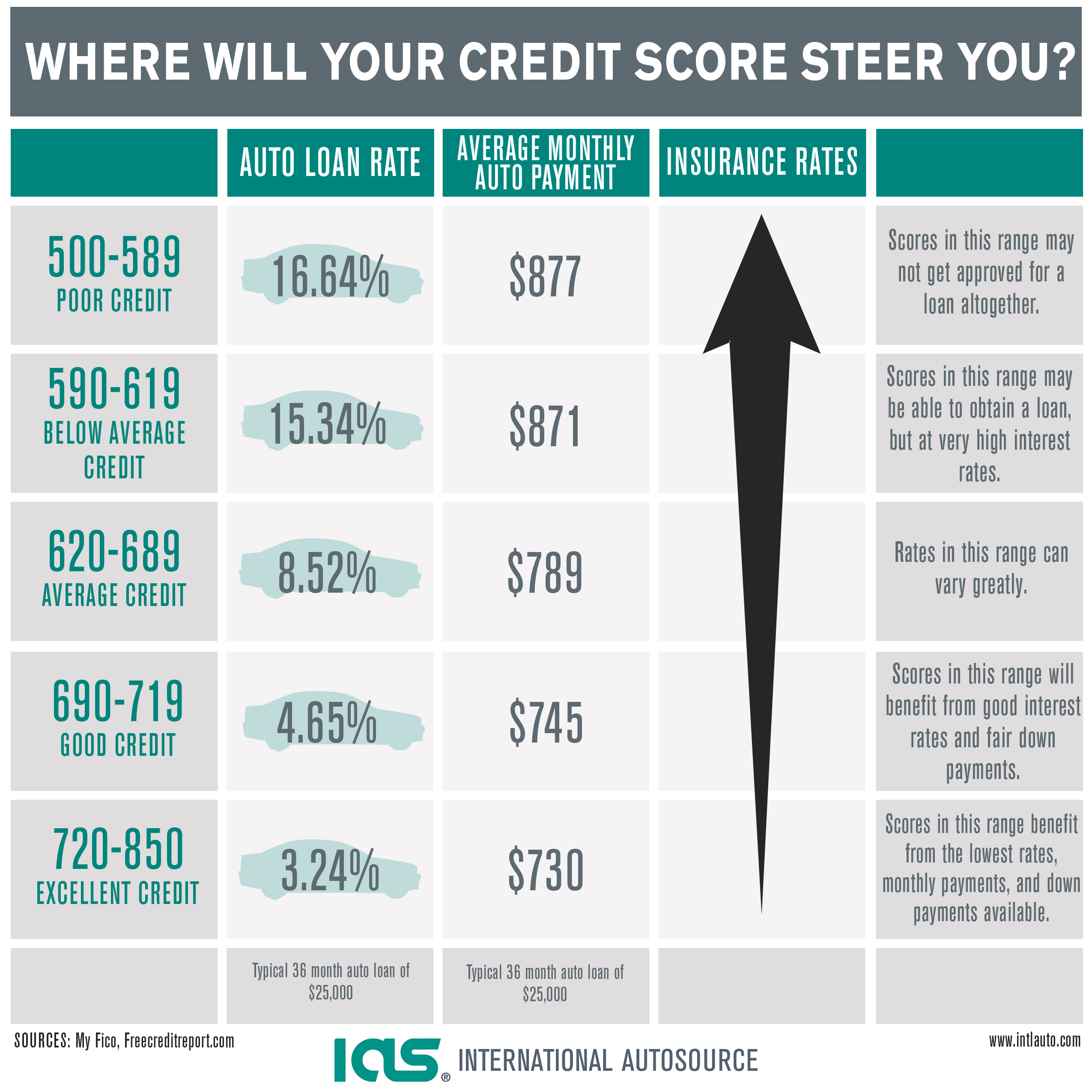

What is Bad Credit?

Credit scores, typically ranging from 300 to 850, are a numerical representation of your creditworthiness. While definitions can vary slightly by lender, generally:

- Excellent: 780-850

- Very Good: 740-779

- Good: 670-739

- Fair: 580-669

- Poor/Bad: 300-579

If your score falls into the "fair" or "poor/bad" categories, lenders perceive you as a higher risk. This risk stems from a history of late payments, defaults, bankruptcies, or a lack of credit history altogether.

Why Lenders Are Hesitant (and How They Compensate)

When you have bad credit, lenders face a higher probability that you might default on your loan. To offset this increased risk, they typically do two things:

- Charge Higher Interest Rates (APR): This is the most significant impact. A higher Annual Percentage Rate (APR) means you’ll pay substantially more over the life of the loan, increasing your monthly payments and the total cost of the vehicle.

- Require Stricter Terms: This could include a larger down payment, a shorter loan term (resulting in higher monthly payments), or even a requirement for a cosigner.

The key takeaway here is that while you can get a loan, it will likely be more expensive than for someone with good credit. Understanding this reality is the first step toward smart decision-making.

Pre-Purchase Preparation: Laying the Groundwork for Success

Success in buying a new car with bad credit hinges on thorough preparation. Don’t walk into a dealership unprepared; do your homework first.

1. Know Your Credit Score and Report Inside Out

Before anyone else pulls your credit, you should. Obtain your credit report from all three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com.

- Check for Errors: Discrepancies or mistakes on your report can unfairly lower your score. Dispute any inaccuracies immediately; correcting them can boost your score quickly.

- Understand Your Score: Identify the factors contributing to your low score. Are there old debts you can settle? Late payments you can address? Even small improvements can make a difference.

2. Budget Realistically (and Beyond the Monthly Payment)

A new car is a significant financial commitment. Don’t just focus on the monthly payment.

- Total Cost of Ownership: Factor in insurance (which might be higher with bad credit), fuel, maintenance, registration, and potential extended warranties.

- Affordability: Determine a comfortable maximum monthly payment based on your income and expenses. Lenders typically prefer your total debt-to-income ratio (DTI) to be below 40%, including the new car payment.

3. Save for a Substantial Down Payment

This is arguably the most critical step for buyers with bad credit. A larger down payment:

- Reduces the Loan Amount: Less money borrowed means lower monthly payments and less interest paid over time.

- Shows Commitment: Lenders view a significant down payment as a sign of your financial commitment and ability to save, reducing their perceived risk.

- Builds Equity Faster: You start with more equity in the car, protecting you against becoming "upside down" on the loan (owing more than the car is worth).

- Recommendation: Aim for at least 10-20% of the car’s purchase price, if not more.

4. Consider a Cosigner (If Necessary)

A cosigner is someone with excellent credit who agrees to take on the responsibility of your loan if you default.

- Benefits: A cosigner can significantly increase your chances of approval and help you secure a lower interest rate.

- Risks: It’s a serious commitment for the cosigner. If you miss payments, their credit score will be negatively affected, and they will be legally obligated to pay the debt. Only consider this if you are absolutely confident in your ability to make payments on time.

Finding the Right Financing: Where to Look for Loans

With bad credit, not all lenders are created equal. You’ll need to know where to focus your search.

1. Start with Online Lenders and Subprime Specialists

Many online lenders specialize in loans for individuals with less-than-perfect credit. They have algorithms designed to assess risk differently.

- Pre-Approval: Many offer pre-approval processes that involve a "soft" credit pull (which doesn’t harm your score) and give you a realistic idea of the interest rate and loan amount you qualify for. Getting pre-approved before stepping into a dealership is crucial. It gives you leverage and a baseline offer to compare.

2. Credit Unions

Credit unions are member-owned financial institutions known for often offering more flexible lending criteria and competitive rates, even for those with lower credit scores, compared to traditional banks.

- Relationship Lending: If you’re already a member, your existing relationship might work in your favor.

3. Dealership Financing (and Understanding the Types)

Most dealerships offer financing, acting as intermediaries between you and various lenders.

- Captive Lenders: These are financing arms of the car manufacturers (e.g., Ford Credit, Honda Financial Services). While they often have attractive deals for good credit, their subprime options might be limited or less competitive.

- Third-Party Lenders: Dealerships also work with a network of banks and finance companies, including those specializing in subprime loans.

- Beware "Buy Here, Pay Here" (for New Cars): While common for used cars, "buy here, pay here" lots typically don’t sell new vehicles. Their business model often involves extremely high interest rates and short repayment terms. If you’re specifically looking for a new car, this isn’t your avenue.

Navigating the Dealership: Your Strategy on the Lot

Once you have your pre-approval in hand and a budget set, it’s time to visit dealerships.

1. Be Upfront About Your Credit Situation

Don’t try to hide your credit score. Be transparent. This saves time and allows the dealer to match you with appropriate lenders from their network. Present your pre-approval offer immediately.

2. Focus on the Out-the-Door Price, Not Just the Monthly Payment

Dealerships often try to negotiate based solely on the monthly payment. This can lead to longer loan terms and higher interest, inflating the total cost.

- Insist on the Total Price: Negotiate the price of the car first, then discuss financing.

- Avoid Add-ons: Resist high-profit add-ons like extended warranties, paint protection, or VIN etching at the point of sale. If you want these, research and buy them separately later.

3. Be Realistic About Your Car Choice

With bad credit, you might not qualify for the most expensive or luxurious models.

- Consider Entry-Level Models: Many manufacturers offer excellent entry-level sedans, hatchbacks, or even smaller SUVs that are more affordable and easier to finance.

- Trim Levels: Opt for a lower trim level with fewer optional features to keep the price down.

4. Don’t Be Afraid to Walk Away

If the terms aren’t favorable, or you feel pressured, be prepared to leave. There are other dealerships and other cars. Your pre-approval gives you the power to walk away confidently.

5. Read Every Document Carefully

Before signing anything, meticulously review all paperwork, especially the loan agreement.

- Verify APR: Ensure the interest rate matches what was agreed upon.

- Check Loan Term: Confirm the number of months.

- Look for Hidden Fees: Understand all charges included in the final price.

The "New Car" Aspect with Bad Credit: A Unique Consideration

While it’s generally easier to get a used car loan with bad credit due to the lower overall price, opting for a new car can still be a strategic move.

- Reliability and Warranty: New cars come with manufacturer warranties, significantly reducing the risk of unexpected repair costs, which can be a major burden for someone with tight finances.

- Latest Technology & Safety: New vehicles offer the most current safety features and infotainment technology.

- Potential for Dealer Incentives: Sometimes, manufacturers offer incentives on new models (cash back, low APR for well-qualified buyers) that can slightly offset the bad credit penalty, though direct bad credit incentives are rare.

However, remember that new cars depreciate rapidly. You’ll need to weigh the benefits of a new car against its higher initial cost and depreciation compared to a reliable, late-model used car.

Table: Impact of Credit Score on a New Car Loan (Hypothetical Example)

Understanding the financial implications is key. This table illustrates how different credit scores can impact a hypothetical new car loan of $36,000 over a 72-month term (6 years), assuming a 10% down payment.

| Credit Score Range | Interest Rate (APR) | Monthly Payment (approx.) | Total Cost of Loan (approx.) | Notes on Financing |

|---|---|---|---|---|

| 720+ (Excellent) | 3.5% – 6.0% | ~$554 – ~$587 | ~$39,888 – ~$42,264 | Best terms, lowest overall cost. |

| 660-719 (Good) | 6.0% – 9.0% | ~$587 – ~$623 | ~$42,264 – ~$44,856 | Still good, but higher rates than excellent. |

| 600-659 (Fair) | 9.0% – 14.0% | ~$623 – ~$691 | ~$44,856 – ~$49,752 | Noticeable increase in cost. |

| 500-599 (Poor/Bad) | 14.0% – 20.0%+ | ~$691 – ~$788+ | ~$49,752 – ~$56,736+ | Significantly higher payments and total cost. May require larger down payment or cosigner. |

| <500 (Very Bad) | 20.0%+ | ~$788+ | ~$56,736+ | Very challenging, often requires large down payment, cosigner, or accepting very high rates. |

Disclaimer: These are hypothetical examples for illustrative purposes. Actual rates and payments vary widely based on individual credit profile, lender, loan term, down payment amount, vehicle price, and current market conditions. Always get multiple quotes.

Practical Advice and Actionable Insights

- Get Pre-Approved: This cannot be stressed enough. It empowers you.

- Save a Large Down Payment: The more you put down, the better your chances and terms.

- Shop Around for Rates: Don’t take the first offer. Compare at least 3-5 lenders.

- Be Realistic: Understand that you’ll pay more for a new car with bad credit.

- Focus on Rebuilding Credit: Make every payment on time. This car loan can be a powerful tool for improving your score for future financial endeavors.

Frequently Asked Questions (FAQ)

Q1: Can I really buy a brand new car with bad credit?

A1: Yes, it is possible, but it will be more challenging and likely more expensive than for someone with good credit. It requires thorough preparation, a substantial down payment, and realistic expectations.

Q2: What’s the best way to get a car loan with bad credit?

A2: The best approach is to get pre-approved by multiple lenders (especially online subprime lenders and credit unions), save a large down payment, and consider a cosigner if possible.

Q3: Will getting a new car loan help improve my credit score?

A3: Absolutely. If you make all your payments on time, consistently and fully, a car loan can significantly help rebuild your credit history and improve your score over time. This is one of the key benefits of successfully managing such a loan.

Q4: How much down payment do I need with bad credit?

A4: While there’s no fixed amount, aiming for 10-20% of the car’s purchase price is highly recommended. The more you can put down, the better your chances of approval and securing more favorable terms.

Q5: Should I use a "buy here, pay here" lot for a new car?

A5: "Buy here, pay here" lots typically sell used vehicles and are generally not recommended for new car purchases. They often come with extremely high interest rates, short repayment terms, and can be predatory. Focus on traditional dealerships and reputable lenders for new cars.

Q6: What’s the biggest impact of a high interest rate on my car loan?

A6: A high interest rate means you will pay significantly more over the life of the loan. Your monthly payments will be higher, and the total cost of the vehicle (principal + interest) will be substantially greater than if you had a lower APR.

Conclusion

Buying a brand new car with bad credit is not a pipe dream, but a financial undertaking that demands careful planning, research, and a strategic approach. While the journey may present hurdles in the form of higher interest rates and stricter terms, it is entirely surmountable. By understanding your credit situation, diligently saving for a down payment, exploring diverse lending options, and negotiating wisely at the dealership, you can turn the key to your new vehicle.

More importantly, successfully managing a new car loan can be a powerful stepping stone towards financial rehabilitation. Each on-time payment you make not only brings you closer to owning your car outright but also steadily rebuilds your credit score, opening doors to better financial opportunities in the future. Embrace the challenge, stay informed, and drive towards a brighter financial horizon.